While I grew up going to Cerruti and Barneys, memories of that time are faint. It’s really in middle school, when memories are more concrete, that there’s some semblance of narrative reliability. Disembarking from the escalators at the end of the wood-paneled lobby onto the second floor, there was the annual back-to-school pilgrimage to Brooks Boys at the 346 Madison Avenue flagship. Larry would be my salesman and I would later see him at the Brooks Brothers store that opened up at 666 Fifth. Although closer to me, the location didn’t quite have the character of 346 Madison. But service was service.

It is this stubborn attachment to a seemingly simpler time that drives the nostalgia of a certain set. Preppy style is, by definition, a nostalgic style, shaped by one’s formative years.

Societal shocks create changes. The rise of khaki can be attributed to its use in wartime being brought into civilian life as veterans returned home. The upheavals in light of the Vietnam War brought about the end of Ivy League style and the rise of hippie style.

Despite the resurgence of preppies as a Reagan era reaction, casualization resumed in the 1990s with the tech boom. Intel pioneered a more egalitarian office culture. The traitorous eight at Fairchild Semiconductor would not have worn suits had they been around at the turn of our century.

The mid-century IBM man—known for his white shirt—became a thing of the past. The PC business at IBM was sold to Lenovo while Apple, influenced by the Whole Earth Catalog, became the story of the aughts. The hippies had won.

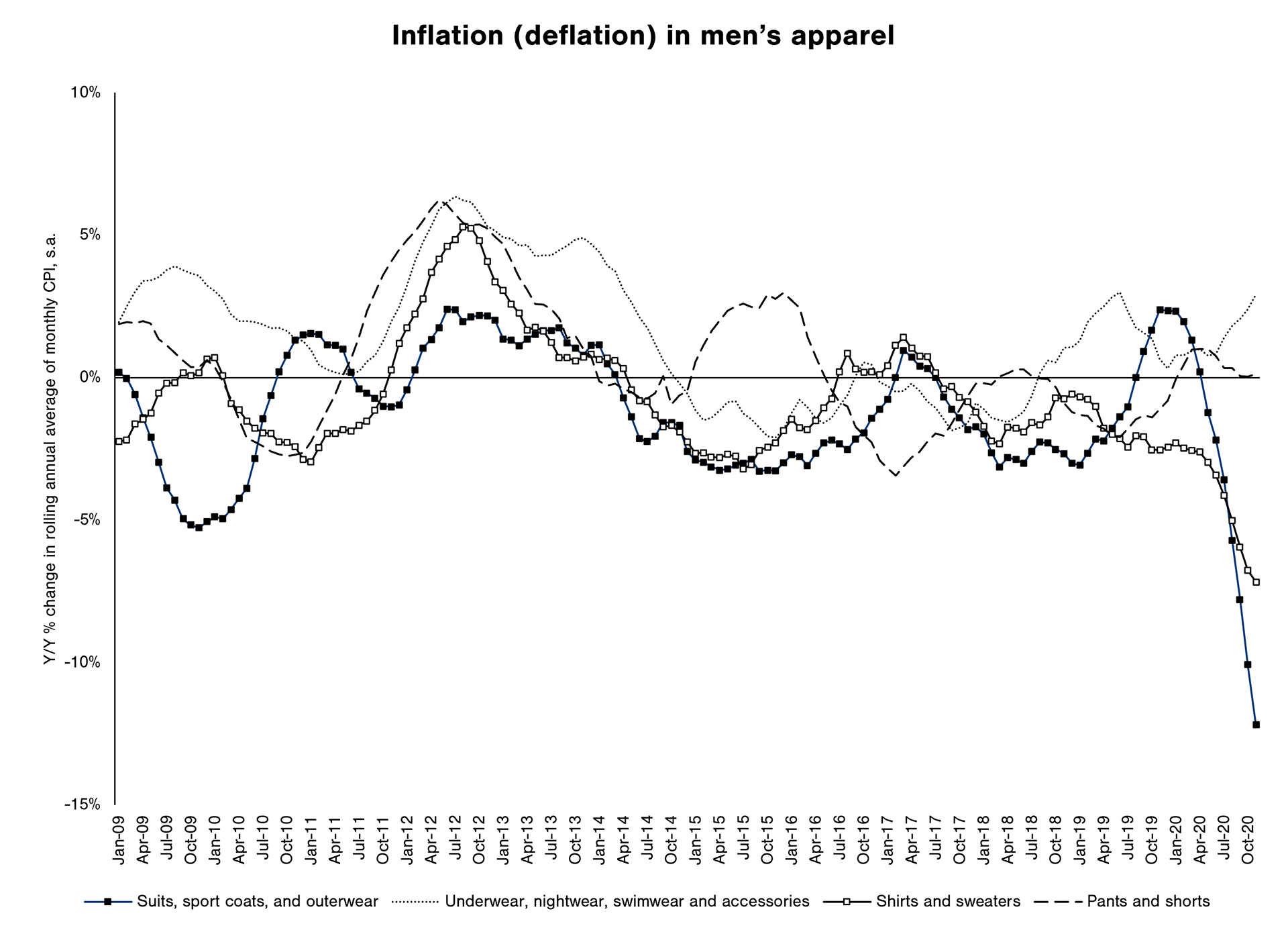

The year without trousers

In 2020, the story was trousers. Or rather, the lack of them. While I haven’t been able to find a dataset that properly separates the longs from the shorts in the pants department, I found the CPI breakouts for these categories:

Graph best viewed in Landscape when using mobile.

Source: BLS. Series CUSR0000SEAA01 to CUSR0000SEAA04, year-over-year change in the 12-month rolling average.

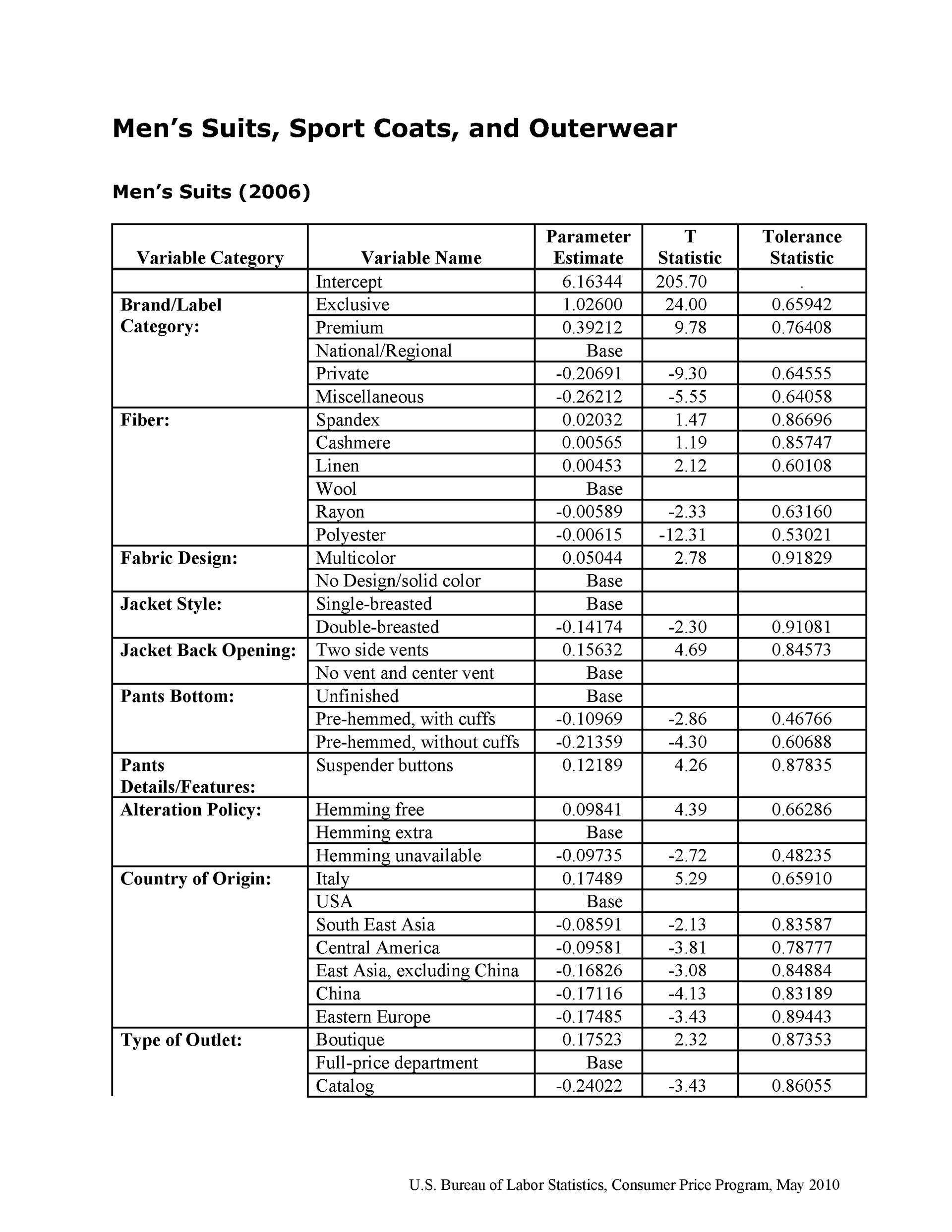

While the huge deflation in suits during 2020 is the most obvious part of this graph, long before then were underlying trends, merely accelerated by the shift to work-from-home. Even prior to this downturn, suits had far more deflationary months than inflationary months. In March 2009, when the S&P 500 reached its nadir, the suit index was at 116.592. In January 2020, more than a decade later, it had gone down to 105.184. In November of this year, it was 85.874.

Source: BLS. Hedonic quality adjustments for the suit series, in case anyone is interested in designing an exclusive spandex (?!) multicolor single-breasted suit with two side vents, suspender buttons, made in Italy, and sold at boutiques.

Secular casualization continued. In the late aughts and early ’10s, Mark Zuckerberg, an Exonian whose most iconic article of clothing is a hoodie, eclipsed the more traditionally clad Instagram founder and Middlesex alumnus Kevin Systrom.

In Japan, long a bastion of Ivy Style, climate change led to the doffing of jackets. Just as we no longer had a need for raccoon coats, Japan no longer had a need for jackets in summer.

Further pressuring apparel companies was a new guard. Usually these new brands start out dominating a single product. Vineyard Vines Americanized the Ferragamo tie. Rowing Blazers was founded by a rower who literally wrote the book on blazers.

New 21st century brands often start direct-to-consumer, but inevitably go omnichannel. As they open brick & mortar locations, they don’t have the same legacy leases that trap older brands. Instead of being stuck in dying malls, they were free to open in vibrant, resurgent shopping drags.

There was also a not-so-new guard rising as well. As the vest became the iconic item of the ’10s, longtime brand Patagonia became the status symbol of the decade.

These have all conspired to take wallet share from the legacy brands, with COVID delivering the coup de grace.

There is still hope. Brands can wane and resurge. I didn’t grow up with IZOD. I came of age in an era dominated by Ralph Lauren, but that’s what made Lacoste so cool when they reentered the American market.

J. Crew started as a catalogue and if it can get out of bad leases, it can retrench. But there’s also the issue of That J. Crew Gingham Shirt. Scale does not per se make it impossible to differentiate—see Apple. But apparel is so tied to identity that ubiquitous brands tend to be incompatible with a differentiation strategy.

What is cool to a subculture is cool because it is unique to that subculture. Subcultures have tribal identifiers that serve as secret handshakes. Once something reaches ubiquity within larger society, it’s no longer cool, no matter the subculture. Nike is ubiquitous, but Boast is cool. Scarcity creates value not simply because of where supply and demand intersect, but also because scarcity induces demand.

What became of J. Crew’s identity? H&M, but preppier? J. Crew ultimately lost pricing power but didn’t have the cost leadership of Zara or H&M, which would have allowed it to survive that loss in pricing power.

Assessing the aftermath

Barneys charged too much and offered too little. I remember looking at dress shirts on the first floor and thinking how I could get custom shirts at Ascot Chang or J. Press for far cheaper. I could probably even get a bespoke shirt from Turnbull & Asser at those prices.

They were also extremely tone deaf in recent years. They had a display of live butterflies at the Beverly Hills store that PETA protested after it had led to the deaths of the butterflies. A few years after the financial crisis, they revealed their Christmas windows with a Baz Luhrmann over-the-top sequence that seemed to be inspired by Marie-Antoinette.

Barneys will live on with two locations slated to open in 2021, one inside Saks in Manhattan and the other as a standalone in Greenwich. Fred’s will return as well. It remains to be seen what will happen to the brand, but with those locations, they’ll have an opportunity to rework the brand under lower stakes.

While I can’t speak for parent company Neiman Marcus, Bergdorf’s still has a reason to exist. It’s part of the Ladies Who Lunch cluster that includes the Palm Court and Breakfast at Tiffany’s. For the Men’s Store, it’s hard to find Kiton and Charvet under one roof. One stop shopping for Moncler and Balenciaga for princelings at Swiss boarding schools.

Bergdorf’s is where I also discovered Master & Dynamic headphones, which are $50 cheaper than AirPods Max headphones from the Apple Store across the street. Yet Master & Dynamics look more like the type of headphones that would be used by someone clad in Brunello Cuccinelli.

Neiman Marcus was, in the end, a casualty of a capital structure built for the good times combined with competition from those more competent at e-commerce like Mr Porter/Net-a-Porter and Matches Fashion. Luxury is ultimately, at the end of the day, resilient. Maisons with capital structures designed with the cyclicality inherent in discretionary fashion in mind have been able to weather this downturn.

As for Brooks Brothers, it’s hard to say what will happen. Simon Property Group and Authentic Brands—the new joint owners of Brooks Brothers (“SPARC”)—have committed to operating 125 stores.

Right now, the website is littered with items that are at least 50% off list. Is this merely attempt to clear inventory that piled up because of work-from-home? Or did they lose inventory discipline before this? They have six pages of colorways for Oxford shirts alone!

Brooks also invested in converting store footage into coffee shops at its Flatiron and 346 Madison locations, then had to shut them once COVID hit. While Ralph Lauren has been extremely successful in the restaurant business—from The Polo Bar being booked solid when it first opened to huge queues outside Ralph’s Coffee even during COVID—Brooks Brothers coffee shops just never generated the same level of buzz.*

*Aside: I recall being served milk & cookies as a kid when shopping at Ralph Lauren’s Rhinelander mansion. Also, if you regularly shopped at Ralph’s, you could get easily get Polo Bar reservations. They know how to do things over there.

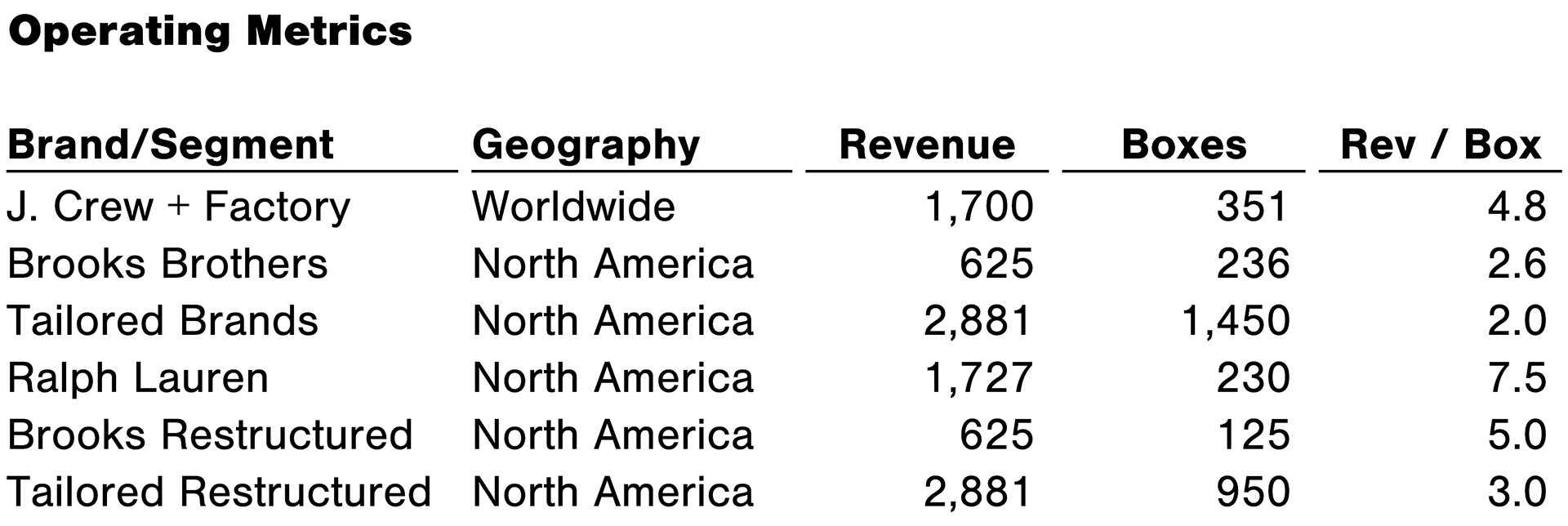

Tailored Brands (parent of Jos. A. Bank and Men’s Wearhouse) and Ralph Lauren don’t explicitly break out digital commerce (RL just breaks out SSS comps) and I wasn’t able to find the square footage for Brooks Brothers as a whole in any public filings so far. But they all disclose a variety of revenue figures with the corresponding number of boxes. So revenue per box is the most comparable operating metric from which to somewhat glean the relative efficiency of Brooks Brothers stores.

Table best viewed in Landscape when using mobile.

Sources: J. Crew First Day Declaration, Brooks Brothers First Day Declaration, Ralph Lauren 8-K, Tailored Brands 10-K and 8-K. For Brooks Brothers, we add what we believe the North American slice is of digital commerce, which is not ideal, but makes it more comparable to Tailored and Ralph. This is all back-of-the-envelope as I’m not actually involved in any of these deals. I’m looking at it from the perspective of a nostalgic client.

We’re looking at $2.6 million per box for Brooks Brothers compared to $2.0 million per box for Tailored Brands. SPARC has committed to operating 125 Brooks Brothers stores while Tailored Brands plans 500 store closures. If each company were to achieve the same revenue with the smaller footprints (they won’t immediately/this is just for illustration), Brooks Brothers revenue per box would rise to $5.0 million while Tailored Brands would rise to $3.0 million. Still, both would pale in comparison to Ralph Lauren’s $7.5 million per box.

This is ultimately a story about brick & mortar overextension. Getting out of bad leases will lower the burn rate and will allow you invest more in the boxes that remain. And bringing back some semblance of exclusivity should bring back pricing power.

Playbook

With the complete implosion of the suit market, where should Brooks Brothers take their products? According to Pauline Brown, the former Chairman of LVMH North America, there are three types of companies: rule makers, rule takers, and rule breakers.

In its early years, Brooks Brothers was a rule breaker. They invented the sack suit. They invented the button-down shirt. By the mid 20th century, they had become a rule maker. By the early 21st century, a rule taker. What will Brooks Brothers be going forward?

What we know so far is Authentic Brands has an ambition to be an LVMH style holding company, though with more of a mass market portfolio. There are some iconoclastic suggestions (Brooks Brothers + Spyder), which feel more like alliances of convenience, borne of what Authentic happens to have under their umbrella.

But ultimately, what Brooks Brothers was doing before clearly wasn’t working. Suitsupply and Indochino were breathing down its neck while the suit market was melting down.

The new Brooks Brothers playbook is encouraging though: it will be a more casual Brooks Brothers, for the country club rather than the office. They’ll streamline SKUs so they can focus on their icons:

In a whiteboard at the new Brooks Brothers offices at 1411 Broadway is the “icon list” that Bastian and the design team created to ensure the signature pieces customers expect to find when they visit the brand are not forgotten. “The customer is really loyal, but there’s been a level of frustration,” he said, when some of the classic items such as the oxford button-down shirt — “Our Levi’s 501s,” Bastian described it — are out of stock.

And they’re scouring the archives to find products that are so old that they’ll be totally new to the current generation.

He’s also found some other eye-openers, such as a chambray jogging suit from the Eighties that he’s reinventing.

“We’re not a trendy brand, but we’ve participated in every trend,” he said. “We believe we can update these things in an authentic way.”

The designer has spent hours scouring the brand’s rich archives and the office is filled with vintage items such as an oxford pop-up from the Forties that is so oversize that it’s “like a dress,” Bastian said with a chuckle. He’s also poring over resale sites for pieces that can fill in the blanks. Case in point is a men’s ascot shirt that will be reinvented in the women’s collection next fall. He’s also “working forensically,” measuring collars and cuffs to “perfect the icons.”

“We’re not reinventing the wheel, we’re just putting the spokes back in,” Bastian said.

Tempora mutantur, nos et mutamur in illis. The times change and we change with it. But also, plus ça change, plus c'est la même chose. The more things change, the more they stay the same.